The IRS issues over 4 million automated notices annually, yet most taxpayers don’t realize that a cp2000 irs letter is a proposed adjustment rather than a final demand for payment. It’s natural to feel overwhelmed by the technical language and the strict 30 day response window. You may worry that a discrepancy between your tax return and third party reporting, like a 1099 or W-2, will trigger a formal audit or lead to a 20% accuracy related penalty. This sense of uncertainty is common, but it doesn’t have to dictate your financial future.

You can regain control by following a methodical, expert led strategy to resolve these discrepancies. This guide explains how to challenge the proposed changes, verify your income records, and protect your finances from interest rates that can reach 7% in 2026. We will walk through the specific steps to address the IRS Automated Underreporter program, prevent state tax complications, and reach a resolution for the lowest possible amount. By understanding the administrative process, you can move from a state of restriction to a state of financial freedom.

Key Takeaways

- Recognize that a CP2000 is a Notice of Proposed Adjustment rather than a final bill; this provides a critical window to verify and contest discrepancies.

- Master the step-by-step process for responding to a cp2000 irs notice to ensure you meet the 30-day deadline and maintain your right to appeal.

- Identify common triggers for automated notices, such as mismatched 1099-B or 1099-K forms, and learn how to provide the evidence needed to correct the IRS record.

- Protect your financial standing by learning how to challenge the 20% accuracy-related penalty and mitigate the impact of daily compounded interest.

- Understand the strategic advantages of professional representation when navigating complex administrative procedures and preventing secondary state-level tax audits.

What is an IRS CP2000 Notice? Understanding the Automated Underreporter Program

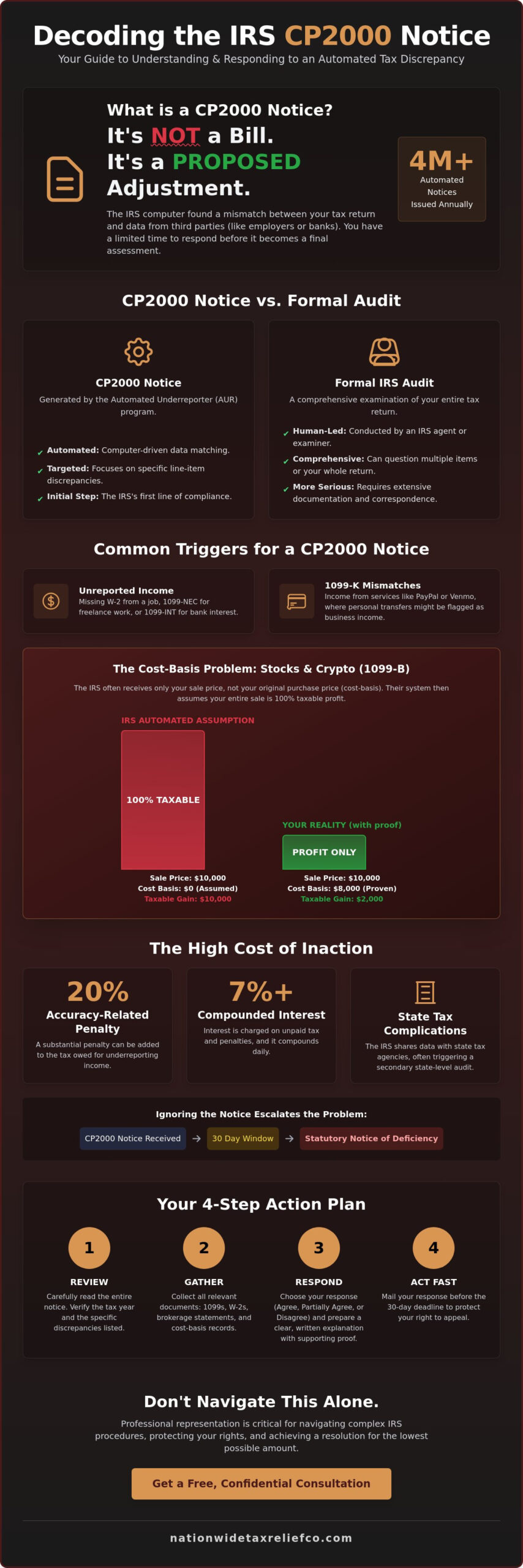

Receiving a letter from the IRS often triggers immediate anxiety, but understanding the specific nature of the document is the first step toward resolution. The cp2000 irs notice is officially titled a “Notice of Proposed Adjustment.” It isn’t a bill or a final demand for payment. Instead, it’s a notification that the information reported on your tax return doesn’t match the data the IRS received from third parties like employers, banks, or brokerage firms. This automated system identifies discrepancies in an effort to close the tax gap, which represents the difference between what taxpayers owe and what the government actually collects.

The Automated Underreporter (AUR) program generates these notices when its algorithms detect a mismatch. You must realize that the “Amount You Owe” listed on the front page is simply the computer’s best guess based on the data available. It doesn’t account for specific deductions, cost basis, or tax credits you might be eligible for. You have a 30-day window from the date printed on the notice to respond. Missing this deadline often leads to the issuance of a formal Statutory Notice of Deficiency, which significantly narrows your options for a favorable outcome.

CP2000 vs. a Formal Audit: Key Differences

While a cp2000 irs notice is serious, it’s technically not a formal tax audit. A formal audit involves a comprehensive examination of your entire return, often requiring an in-person meeting or extensive mail correspondence regarding multiple line items. In contrast, the AUR process is a targeted matching program. It focuses specifically on line items where a 1099 or W-2 mismatch exists. Essentially, AUR serves as the IRS’s first line of automated compliance enforcement.

Common CP2000 Notice Variants (CP2000A, B, C)

You may encounter variations such as the CP2000A, which is often used for amended returns or specific follow-ups. If you provide new information or challenge the initial findings, the IRS might issue a revised CP2000 to reflect the updated calculations. Always verify the tax year listed in the top right corner of the notice. Discrepancies often surface one to two years after a return is filed, so ensuring you’re reviewing the correct records is vital for an accurate defense. This verification prevents you from inadvertently responding to a notice regarding a different tax period than the one under review.

Why You Received a CP2000: Common Discrepancy Triggers

The IRS receives millions of information returns from third parties every year. When the income figures on your Form 1040 don’t align with these records, the Automated Underreporter (AUR) system flags the return for review. This is the primary reason for receiving a cp2000 irs notice. According to IRS Topic No. 652, this document outlines the specific differences between what you reported and what the IRS received from sources like your employer or bank.

Common sources of error include 1099-B forms for brokerage transactions and 1099-K forms for payment card and third-party network transactions. If you had a short-term side hustle or seasonal employment, a missing W-2 can also trigger a notice. The IRS computer is highly efficient at spotting these omissions. It doesn’t matter if the missing income was $50 or $50,000; the system is designed to identify every mismatch.

The Cost-Basis Problem in Crypto and Stock Trading

Cryptocurrency and stock trades often lead to significant proposed tax bills because of how the IRS calculates gains. If a platform issues a 1099-B or the new 1099-DA but fails to report your original purchase price, the IRS lacks the data to calculate your actual profit. “The IRS computer assumes your entire sale price is taxable profit unless you prove otherwise with cost-basis documentation.” This often results in a proposed tax liability that is far higher than what you actually owe.

Similar issues arise with 1099-K reporting from processors like Venmo or PayPal. If personal transfers are incorrectly flagged as business income, you’ll receive a notice for unreported revenue. Resolving these complex data mismatches often requires a structured IRS personal tax audit defense to ensure you only pay what is legally required. A methodical review of your transaction history is essential to correct these automated assumptions.

Retirement Distributions and Educational Credits

Retirement account activity is another frequent trigger for a cp2000 irs notice. If you performed a tax-free rollover but the 1099-R wasn’t coded correctly, the computer flags the entire distribution as taxable income. Educational credits also face scrutiny. If the 1098-T from a university doesn’t match the amounts claimed on your return, a notice is almost certain. These errors are usually procedural, but they require technical documentation to resolve.

Finally, don’t overlook gambling winnings reported on Form W-2G. The IRS tracks these closely. If you don’t report the gross winnings, even if you had offsetting losses, the AUR system will generate a notice. Systematic verification of every third-party form is the only way to prevent these automated challenges. Providing the IRS with the correct context for these payments can often eliminate the proposed debt entirely.

How to Respond to a CP2000 Notice: A Step-by-Step Defense

Responding to a cp2000 irs notice requires a meticulous and disciplined approach to ensure your rights are protected. The document provides a detailed breakdown of the discrepancies found by the Automated Underreporter system. Your first action must be a side-by-side comparison of the “IRS Records” column against your own personal tax files and third-party documents. This verification process allows you to pinpoint exactly where the computer’s logic fails to account for your actual financial situation.

Once you’ve identified the source of the mismatch, you must categorize your response into one of three positions: Agree, Partially Agree, or Disagree. For those who disagree, gathering contemporaneous documentation is the most critical phase of your defense. This includes obtaining corrected 1099 forms from the original issuer, bank statements, or receipts that prove the income was either previously reported or non-taxable. According to the official guidance on Understanding Your CP2000 Notice, providing clear evidence is the only way to reverse the proposed assessment.

After compiling your evidence, draft a concise formal statement that addresses each disputed line item individually. Avoid emotional language; focus strictly on the facts and the tax law that supports your position. Finally, use the IRS Document Upload Tool for submission. This digital method provides an immediate confirmation of receipt and a clear paper trail, which is far more reliable than traditional mail when facing a strict 30-day deadline.

Agreeing with the Notice: What Happens Next?

If your review confirms that the IRS findings are accurate, you may choose to sign the “Agree” section of the response form. It’s vital to understand that signing this document waives your right to challenge these specific issues in U.S. Tax Court later. Before signing, review the notice for any accuracy-related penalties. If you truly owe the debt but cannot pay in full, you can request a payment plan or installment agreement to manage the balance. However, don’t agree simply to end the process if you believe the computer has made an error in its calculations.

Disagreeing with the IRS: The Burden of Proof

When you disagree with the cp2000 irs findings, the burden of proof rests entirely on you. You must provide a “Statement of Disagreement” that clearly outlines why the proposed changes are incorrect. One common mistake is filing an amended return (Form 1040-X) for the year in question. You should generally avoid filing a 1040-X while a CP2000 is pending unless the notice specifically instructs you to do so, as it can confuse the AUR unit and delay your resolution. Use the unique Access Code provided on your notice to upload your disagreement statement and supporting documents directly to the IRS portal for the fastest processing.

The Risks of Mishandling a CP2000: Penalties and State Taxes

Ignoring a cp2000 irs notice is a costly mistake that often leads to a rapid escalation of your total tax liability. When the Automated Underreporter system identifies a substantial understatement of tax, the IRS typically assesses a 20% accuracy-related penalty. This isn’t the only financial burden you’ll face. For the first and third quarters of 2026, the interest rate on underpayments is 7%, while the second quarter sits at 6%. Because this interest compounds daily, a delay of even a few months can increase your balance by thousands of dollars. Business owners facing similar escalating penalties should also explore professional business tax audit defense strategies to protect their company assets from IRS collection actions.

If you fail to respond within the initial 30-day window, the IRS will issue a Statutory Notice of Deficiency, also known as a CP3219A. This document provides a final 90-day period to petition the U.S. Tax Court. Once this secondary deadline passes, the proposed tax becomes a formal assessment. At this stage, the IRS moves from proposing changes to active collection efforts, which may include levies or liens. The protective window for negotiation effectively closes, leaving you with far fewer options to reduce the debt or challenge the findings.

California FTB and CDTFA Implications for LA Residents

Los Angeles residents must be particularly aware of the robust data-sharing agreement between the IRS and the California Franchise Tax Board (FTB). Once the IRS finalizes an adjustment to your federal return, that information is automatically transmitted to state authorities. You will likely receive a Notice of Proposed Assessment from the FTB shortly after. Even if you resolve the federal discrepancy, you must still address the state-level fallout to prevent separate collection actions. Our team at Nationwide Tax Relief specializes in IRS personal tax audit defense and state-level representation to ensure a comprehensive resolution for both jurisdictions.

Penalty Abatement: Can You Get the Fees Removed?

It is possible to have accuracy-related penalties removed through a process called penalty abatement. Unlike the First-Time Abate policy, which typically applies to failure-to-file or failure-to-pay penalties, accuracy-related penalties triggered by a cp2000 irs notice require you to meet the Reasonable Cause standard. You must demonstrate that you acted in good faith and had a legitimate reason for the reporting error, such as reliance on a faulty third-party document or a complex technical mistake. A methodical defense that highlights these factors can successfully shield you from the 20% surcharge, provided you present the argument before the assessment becomes final.

Why Professional Representation is Critical for CP2000 Disputes

The technical language used in a cp2000 irs notice is designed for administrative efficiency, not for the average taxpayer’s ease of understanding. This “IRS-speak” often masks the specific procedural levers you must pull to reach a favorable resolution. A professional representative translates these dense regulatory requirements into a structured, actionable plan. By establishing a disciplined communication channel with the Automated Underreporter (AUR) unit, an expert ensures that your evidence is presented in a format the IRS is prepared to accept, effectively leveling the playing field between you and the federal government.

One of the most significant dangers of self-representation is the “audit trap.” A poorly structured response or an accidental admission of reporting errors can provide the IRS with justification to expand their inquiry. What began as a simple matching discrepancy could evolve into a comprehensive IRS personal tax audit that examines every line item of your return. Professional advocates act as a protective shield, containing the scope of the inquiry to the specific issues identified in the notice. From our headquarters in Encino, California, we represent clients across all 50 states, ensuring that federal inquiries do not spiral into wider financial examinations.

When a CP2000 Requires an Expert Advocate

Certain scenarios demand a high level of technical precision that goes beyond basic record-keeping. If your notice involves complex cryptocurrency transactions and the new 1099-DA forms, the potential for cost-basis errors is exceptionally high. High-net-worth individuals and those with significant business income also face a greater risk of accuracy-related penalties. Self-representation in these high-stakes cases often leads to unnecessary payments because taxpayers don’t know how to argue for the removal of fees based on reasonable cause. Having a steady hand in a crisis ensures that every technical nuance of the tax code is used to your advantage; this methodical approach prevents the loss of capital due to automated computer errors. Companies and self-employed individuals with more complex tax situations may also benefit from dedicated business tax audit defense to safeguard their operating capital and prevent debilitating liens.

Nationwide Tax Relief: Your Partner in Resolution

Nationwide Tax Relief specializes in navigating the intricate administrative procedures required for audit defense and complex tax resolution. We provide a meticulous review of your notice and supporting documentation before any response is submitted to the IRS. This proactive verification process identifies the most effective path toward a resolution for the lowest possible amount. Rather than reacting to the pressure of a 30-day deadline, we guide you through a systematic roadmap toward financial recovery. You don’t have to face regulatory challenges alone when you have a methodical expert who knows exactly which lever to pull in your specific situation.

Secure Your Financial Future and Resolve Your IRS Discrepancy

Managing a cp2000 irs notice requires a combination of technical precision and timely action. You’ve learned that this document is a proposal rather than a final assessment, which provides a vital opportunity to challenge automated errors with documented facts. By verifying your records against the findings of the Automated Underreporter unit and providing a structured response, you can effectively mitigate accuracy-related penalties and prevent the escalation of daily compounded interest. Documentation is your strongest defense against computer generated assumptions.

Our team at Nationwide Tax Relief acts as a formidable shield between you and the IRS. We provide expert IRS audit representation and specialize in resolving complex crypto and small business tax problems. From our Los Angeles headquarters, we serve clients in all 50 states, ensuring that federal disputes don’t lead to unnecessary financial loss or state level complications. You don’t have to navigate this regulatory challenge alone. A methodical approach ensures you reach a resolution for the lowest possible amount and move forward with total peace of mind.

Get Expert Help Resolving Your CP2000 Notice Today

Frequently Asked Questions

Is a CP2000 notice an audit?

No, a CP2000 is technically a Notice of Proposed Adjustment rather than a formal tax audit. It’s generated by the Automated Underreporter program when computer algorithms detect a mismatch between your return and third party data. While it’s less invasive than a full examination, it functions as a targeted inquiry that can lead to a formal audit if the discrepancies aren’t resolved through proper documentation.

What happens if I ignore an IRS CP2000 notice?

Ignoring this notice allows the IRS to formally assess the proposed tax, interest, and penalties without further input from you. The agency will eventually issue a Statutory Notice of Deficiency (CP3219A), which starts a 90 day clock to petition the U.S. Tax Court. Once that window closes, the IRS can initiate aggressive collection actions, including bank levies or wage garnishments, to recover the balance.

Can I pay a CP2000 notice in installments?

Yes, you can request an installment agreement if you agree with the proposed changes but lack the liquid capital to pay in full. It’s vital to respond to the cp2000 irs notice to establish the final balance before setting up a plan. Establishing an official agreement can reduce the failure to pay penalty from 0.5% to 0.25% per month while protecting you from broader collection efforts.

How long does the IRS take to process a CP2000 response?

The IRS generally takes 60 to 90 days to review and process your response, although peak tax seasons can extend this timeframe. You’ll receive a notification letter, such as a CP2005 or CP2006, once the AUR unit reaches a determination. Using the digital Document Upload Tool is the most efficient way to submit evidence and often results in faster processing than traditional paper mailings.

Should I file an amended return if I get a CP2000?

You should generally avoid filing an amended return (Form 1040-X) for the year in question unless the notice specifically instructs you to do so. Filing an extra return while a CP2000 is pending can cause significant confusion within the AUR system and delay your resolution. Instead, use the response form provided with the notice to explain your position and provide the necessary supporting evidence.

What if the 30-day deadline for my CP2000 has already passed?

If the 30 day window has expired, you must still submit your response immediately to mitigate further interest accumulation. The IRS may still consider your documentation if the tax hasn’t been formally assessed and the Statutory Notice of Deficiency hasn’t been issued. Acting quickly is essential to maintain your rights and prevent the case from moving into the more restrictive 90 day Tax Court petition phase.

Can the IRS be wrong about a CP2000 notice?

Yes, the IRS is frequently incorrect because the cp2000 irs system relies on automated data matching without human context. For instance, the computer often assumes a $0 cost basis for stock or crypto sales, which leads to a massive overstatement of taxable profit. Providing corrected 1099s or transaction logs often proves the computer’s logic was flawed and can eliminate the proposed debt entirely.

Will a CP2000 notice affect my state taxes?

Yes, any final adjustments made to your federal tax return are automatically shared with state taxing authorities like the California Franchise Tax Board. Once the federal assessment is finalized, the state will likely issue its own Notice of Proposed Assessment for the corresponding state tax. Resolving the federal discrepancy with precision is the only way to shield yourself from secondary state level penalties and interest charges.